Back in June 2011, Zero Hedge first posted:

which we followed up on various occasions, most notably with

- “How The Fed’s Latest QE Is Just Another European Bailout” and

- “The Fed’s Bailout Of Europe Continues With Record $237 Billion Injected Into Foreign Banks In Past Month.”

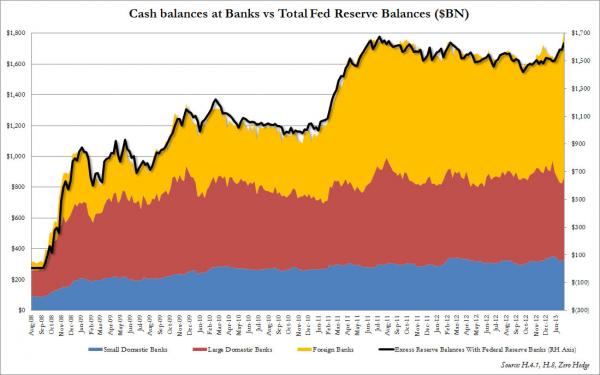

With the following key chart:

Of course, the conformist counter-contrarian punditry, for example the FT’s Alphaville, promptly said this was a non-issue and was purely due to some completely irrelevant microarbing of a few basis points in FDIC penalty surcharges, which as we explained extensively over the past 3 years, has nothing at all to do with the actual motive of hoarding Fed reserves by offshore (or onshore) banks, and which has everything to do with accumulating billions in “dry powder” reserves to use for risk-purchasing purposes (alas understanding that would require grasping that reserves are perfectly valid collateral to use as margin against purchase of such market moving products as e-mini futures, which in turn explains why traders usually don’t end up as journos).

Fast, or rather slow, forward to today when none other than the WSJ’s Jon Hilsenrath debunks yet another “conspiracy theory” and reveals it as “unconspiracy fact” with “Fed Rate Policies Aid Foreign Banks: Lenders Pocket a Spread by Borrowing Cheaply, Parking Funds at Central Bank“

Wait… the Wall Street Journal said that? Yup.

Banks based outside the U.S. have been unlikely beneficiaries of the Federal Reserve’s interest-rate policies, and they are likely to keep profiting as the Fed changes the way it controls borrowing costs.

Foreign firms have received nearly half of the $9.8 billion in interest the Fed has paid banks since the beginning of last year for the money, called reserves, they deposit at the U.S. central bankaccording to an analysis of Fed data by The Wall Street Journal. Those lenders control only about 17% of all bank assets in the U.S.

Moreover, the Fed’s plans for raising interest rates make it likely banks will see those payments grow in coming years.

Hmm, we almost feel like we should bring up the dreaded “P” word considering the bolded sentence is a recap of what we said in February of 2013 in “How The Fed Is Handing Over Billions In “Profits” To Foreign Banks Each Year.” That’s ok, though: imitation, flattery and all that…

So here is Hilsy “figuring out” what we have been explaining for over 3 years!

Though small in relation to their overall revenues, interest payments from the Fed have been a source of virtually risk-free returns for foreign banks. Large holders of Fed reserves include Deutsche Bank, UBS AG, Bank of China and Bank of Tokyo-Mitsubishi UFJ, according to bank regulatory filings. U.S. banks including J.P. Morgan Chase, Wells Fargo and Bank of America Corp. are also big recipients of Fed interest payments, according to the filings.

“It is a small transfer from U.S. taxpayers to foreign taxpayers,” said Joseph Gagnon, a former Fed economist at the Peterson Institute for International Economics. The transfer, he added, was a side effect of Fed policy, not a goal.

Actually it is a goal, but that would lead to a whole lot of embarrassing congressional hearings which the Fed would rather avoid, plus nobody really “gets” it. The reason why? Apparently things are so “complex” that anyone who figured it out years ago was clearly a conspiracy theorist:

Behind the payments is a complex interplay between new government regulatory policies and new methods the Fed has developed to control short-term interest rates.

The Fed has pumped nearly $3 trillion into the banking system since the 2008 financial crisis, increasing banks’ reserves, in efforts to stabilize markets and boost economic growth.

Since 2008, it has paid banks interest of 0.25% on those reserves. The Fed affirmed this month that the rate it pays on reserves will be the primary tool it uses to raise short-term borrowing costs from near zero when the time comes, likely next year.

In part because regulatory requirements discourage domestic banks from holding more cash reserves than they need, many of the reserves created by the Fed are held by foreign banks.

In other words, the Fed-funded risk-free carry trade finally goes mainstream. Of course, all those who read ZH in 2011 will know all of this by now:

The interest payments totaled $4.7 billion so far this year and $5.1 billion last year, and will increase over time as the Fed raises rates. The Fed remits most of its profits to the U.S. Treasury, and the rising cost of the interest payments could put downward pressure on the amount the central bank sends to taxpayers each year, the Fed has said.

Some observers say this could become a political challenge for the Fed, especially the payments it makes to foreign banks.

“The fact is that the Fed is going to be paying very large amounts of interest to banks,” said William Poole, a senior fellow at the Cato Institute and former president of the Federal Reserve Bank of St. Louis. “It’s highly likely that some politicians will notice that and given the proclivity of some politicians anyway to demagogue issues, the Fed is going to have some political explaining to do.”

Some Fed officials also have expressed concern about how these payments will look. “I think the optics are very difficult to defend and might get us into trouble,” James Bullard, president of the Federal Reserve Bank of St. Louis, said in an August interview with MarketWatch.

Since 2009, foreign banks have earned roughly $5 billion by borrowing dollars cheaply, often at less than 0.10%, in short-term funding markets and depositing those funds at the Fed for 0.25%, according to the Journal analysis. That estimate doesn’t take into account the costs of raising money through other means, overhead and taxes, which affect net income.

But don’t blame the banks – they are merely doing what the Fed is encouraging them to do. And after all who wouldn’t collect billions in risk free cash?

A spokeswoman for one bank engaged in the trade, Bank of Tokyo Mitsubishi, said that the growth of excess reserves parked at the central banks is a natural consequence of the Fed’s policy. “The share of excess reserve balances held by BTMU has been in alignment with its business footprint in the U.S.,” she said.

Deutsche Bank, which had one of the largest reserve balances at the Fed as of June 30, declined to comment. UBS didn’t respond to requests for comment. A Chinese official close to Bank of China said it has been parking funds at the Fed in order to help it comply with liquidity requirements in its home market.

The foreign banks’ activity is “entirely legitimate because they are providing a financial service and they are taking a spread,” said Lou Crandall, chief economist at research firm Wrightson ICAP.

Sadly, the WSJ ends just before it gets good. So without further ado, here is what happens if and when one extrapolates a rising rate environment in terms of Fed handouts to foreign banks, from what we said in February of 2013:

We show the surge in the foreign bank cash level, as well as the cumulative cash interest paid to these banks assuming a weekly cash interest payment. What the chart shows is that from December 2008 through the last week of January, the Fed has paid out some $6 billion in cash (red line) to European banks simply as interest on excess reserves.

But that’s just the beginning. If we are correct in assuming that QE3 will be a replica of QE2 when all the new reserves created ended up as cash on foreign bank balance sheets, it means that we can quite accurately forecast what the total foreign bank cash position will be on December 31, 2013 (as the Fed will certainly not end its open ended monetization of the US deficit before then, or likely, ever). The result: just under $2 trillion in cash held be foreign banks operating in the US, which also means that in calendar 2013, the Fed will fund and subsidize foreign banks a blended interest payment of $3.5 billion! This is entirely separate from the $2 trillion liquidity subsidy that Bernanke will also have handed out to keep these banks afloat, and is $3.5 billion that will flow right through the P&L and end up in the pockets of offshore shareholders who otherwise would very likely be wiped out had it not been for the Fed’s relentless efforts to bailout foreign banks.

And since it is improbable that excess reserves held by any banks will decline at all in the coming years, one can also assume that the annualized interest paid to foreign banks, which would amount to at least $5 billion pear year, every year, will continue indefinitely as a direct Fed subsidy to the bottom line of Foreign banks.

All of this, of course, ignores what happens should the Fed hike interest rates across the board, which will also mean rising the rates on IOER, once inflation finally strikes: simple math means a 1% IOER means some $20 billion in interest paid to foreign banks, 2% – $40 billion,5% – $100 billion paid to foreign banks, and so on. Putting these numbers in perspective, let’s recall that Italy’s third largest bank just got a €3.9 billion bailout (its third), and has a market cap of some €2.9 billion.

We can only hope someone in Congress asks Ben Bernanke in two weeks just under which Fed charter it is that the Fed is more focused on generating profits (not just trillions in excess liquidity) for European banks, than on opening up consumer lending which has been stuck in “petrified” mode for the past 4 years, with the total amount of loans outstanding currently at all US banks – foreign and domestic – at levels last seen the week Lehman filed for bankruptcy.

Obviously, nobody asked Bernanke and nobody has asked Yellen this simple question, because until last night apparently nobody aside from the Zero Hedge community had any grasp of what is going on.

That said, we doubt that anyone in control will ask any related questions in the near of not so near future even with Hilsenrath’s “How The Fed Is Bailing Out Foreign Banks For Dummies” primer, because let’s not forget – the same banks that control the Fed are also the same banks that purchase politicians at every possible opportunity (see for example: With Cantor Down, Which Other Politicians Has Goldman Invested In?).

In fact, the only good news from Hilsenrath’s report is that yet another conspiracy theory has been documented as unconspiracy fact. Then again, Zero Hedge readers knew all of this over three years ago, for free.

{kind=link}

Sign up on lukeunfiltered.com or to check out our store on thebestpoliticalshirts.com.